The Greatest Guide To Paul B Insurance Medicare Advantage Agent Huntington

Table of ContentsThe Basic Principles Of Paul B Insurance Medicare Agent Huntington Facts About Paul B Insurance Medicare Supplement Agent Huntington Uncovered

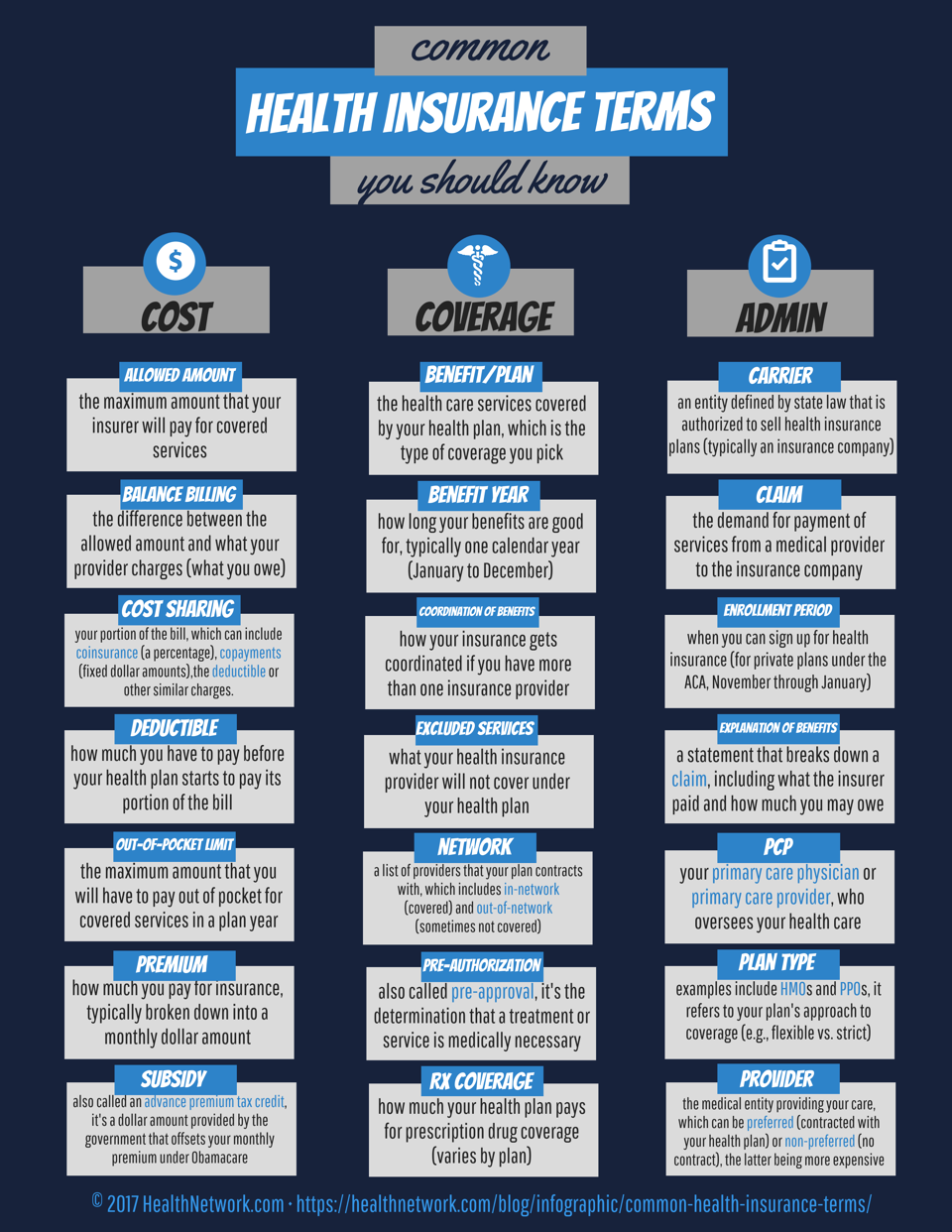

Health insurance plan pay specifies amounts for clinical costs or therapy and also they can offer numerous choices and differ in their strategies to insurance coverage. For assist with your particular concerns, you might want to speak with your companies advantages department, an independent expert consultant, or contact MIDs Consumer Providers Department. Acquiring health and wellness insurance coverage is a really important decision (paul b insurance Medicare Advantage Agent huntington).

Numerous have a tendency to base their entire insurance policy acquiring choice on the premium quantity. As getting a good value, it is additionally really important that you deal with a firm that is economically secure. There are numerous various kinds of wellness insurance. Typical insurance coverage commonly is called a"fee for service "or"indemnity"plan. If you have conventional insurance coverage, the insurance company pays the costs after you obtain the solution. Taken care of care plans use your month-to-month

settlements to cover the majority of your medical costs (paul b insurance Medicare Advantage Agent huntington). Health Care Organizations(HMOs) and Preferred Carrier Organizations(PPOs )are one of the most typical took care of care companies. Handled treatment plans motivate and in some situations call for customers to utilize medical professionals as well as health centers that belong to a network. In both conventional insurance policy and handled treatment strategies, customers might share the expense of a solution. This cost sharing is.

often called a co-payment, co-insurance or deductible. Various terms are made use of in reviewing health and wellness insurance policy. "Suppliers"are physicians, healthcare facilities, pharmacies, labs, urgent treatment centers and other healthcare facilities and also experts. Whether you are taking into consideration signing up in a standard insurance policy plan or managed care strategy, you must know your

legal civil liberties. Mississippi legislation requires all insurance providers to clearly as well as truthfully divulge the following details in their insurance plan: A total checklist of things as well as solutions that the wellness care strategy spends for. State laws restrict how lengthy preexisting condition exemption durations can be for specific and team health and wellness plans. If you have a team health insurance plan, a pre-existing problem is a wellness problem for which clinical advice, diagnosis, care or therapy was advised or gotten within 6 months of signing up witha plan. If you have a private plan, a pre-existing condition is a health and wellness problem for which medical recommendations, diagnosis, treatment or treatment was suggested or obtained within 12 months of joining your strategy. Your plan might reject to pay for solutions connected to your pre-existing problem for twelve month. You may not need to offer a pre-existing problem exclusion duration if you are able to get credit rating for your health treatment coverage you had prior to you joined your new plan. Ask your strategy for even more information. Your health and wellness insurance company must renew your strategy if you desire to restore it. The insurer can not cancel your plan unless it draws out of the Mississippi market completely, or you dedicate fraudulence or abuse or you do not pay your premiums. All health care strategies need to have created treatments for obtaining and also fixing complaints. Grievance procedures need to be regular with state legislation requirements. If your health insurance firm has actually refused to spend for healthcare solutions that you have gotten or intend to get, you have the right to understand the specific contractual, medical or other reason that. If you have an issue concerning a health and wellness insurance firm or an agent, please describe our Data an Issue Web Page. Nevertheless, bear in mind that when you are comparing business as well as requesting the variety of issues that have been submitted against a company, you have to understand that generally the business with the most plans active will have extra problems than firms that just have a couple of plans in place. Every managed care plan should file a summary of its network of service providers and how it makes certain the network can supply healthcare solutions without unreasonable hold-up. In some cases, a doctor, health center, or other healthcare center leaves a managed care strategies network. When this occurs, a managed treatment strategy must alert you if you saw that company on a routine basis.

:max_bytes(150000):strip_icc()/how-much-does-health-insurance-cost-4774184_V2-f7ab6efc9c5042d3aedcbc0ddfc6252f.png)

You have to obtain this list when you enlist, re-enroll, visit site or upon demand. Every handled treatment plan need to maintain close track of the high quality of the healthcare solutions it provides. Handled care strategies should not use benefits or penalties that motivate less treatment than is clinically needed. If you wish to know more concerning just how your plan pays its service providers, you should ask. The notification needs to consist of the major factors for the rejection as well as instructions on just how to appeal. Every handled treatment strategy need to follow specific procedures if it identifies that a healthcare solution was not medically required, efficient, efficient or proper. The procedures have to be totally defined in the certification of protection or participant handbook. You must make a checklist of your requirements to contrast with

The Basic Principles Of Paul B Insurance Medicare Advantage Agent Huntington

the advantages supplied by a strategy you are considering. You ought to contrast strategies to locate out why one is more affordable than one more. Detailed below are some concerns you should ask when buying medical insurance: What does the plan spend for as well as not spend for? Will the plan spend for preventative care, immunizations, well-baby care, chemical abuse, body organ transplants, vision care, oral treatment, the inability to conceive therapy, or long lasting medical tools? Will the plan spend for any prescriptions? If it pays for some, will it pay for all prescriptions? Does the strategy have mental wellness benefits? Will the plan spend for long term physical treatment? Not all plans cover every one of the benefits provided above. Do rates increase as you age? Exactly how typically can prices be changed? Exactly how a lot do you need to pay when you get health and wellness treatment solutions(co-payments as well as deductibles)? Exist any kind of restrictions on just how much you must spend for healthcare services you obtain(out of pocket optimums)? Are there any kind of restrictions on the variety of times you may get a service(life time optimums or yearly advantage caps)? What are the constraints on making use of companies or services index under the plan? Does the health insurance require you to.

see providers in their network? Does the health insurance plan pay for you to see a doctor or use a healthcare facility outside the network? Are the network carriers conveniently located? Is the medical professional you desire to see in the network approving new individuals? What do you need to do to see a professional? How very easy is it to obtain a visit when you require one? Has the business had an abnormally high number of consumer problems? What occurs when you call the companys consumer problem number? For how long does it take to reach a real person? Couples in situations where both spouses are provided medical insurance with their tasks should contrast the insurance coverage as well as costs(costs, co-pays and deductibles)to establish which plan is best for the family members. Keep all invoices for clinical solutions, whether in -or out-of-network (paul b insurance medicare agent huntington). In the occasion you surpass your deductible, you may certify to take a tax obligation reduction for out-of-pocket medical expenses. Think about opening up a Flexible Spending Account (FSA ), if your company provides one, which enables you to allot pre-tax bucks for out-of-pocket medical costs. : that might not yet have a full-time job that offers health benefits need to be mindful that in an expanding number of states, single adult dependents may be able to continue to get wellness coverage for an extended duration( varying from 25 to 30 years old)under their moms and dads 'health insurance plans even if they are no much longer full time students. with kids should think about Flexible Investing Accounts if available to aid spend for usual youth clinical issues such as allergy examinations, braces and substitutes for lost eyeglasses, retainers and also the like, which are frequently not covered by basic health and wellness insurance coverage

All employees who shed or transform jobs must know their civil liberties to continue their health coverage under COBRA for as much as 18 months. At this life stage, customers may wish to evaluate whether they still need handicap insurance. Many will wish to decide whether lasting treatment insurance makes good sense for them(e. g., will they be able to afford the costsright into aging, when most need to make use of such insurance coverage). If we can be useful, please see the Demand Aid Page for information on how to call us. Medical insurance is essential to have, however it's not always very easy to recognize. You may have to take a few actions to make certain your insurance will spend for your healthcare costs. There are likewise a lot of vital words and also expressions to keep straight in your head. Here's some standard information you require click this to know: Wellness insurance assists spend for your health care. It also covers numerous preventive solutions to maintain you healthy and balanced. You pay a month-to-month bill called a costs to acquire your health insurance coverage and you may need to pay a part of the price of your care each time you obtain medical solutions. Each insurance provider has various guidelines for utilizing wellness treatment advantages. Generally, you will certainly give your insurance policy infoto your medical professional or hospital when you choose treatment. The doctor or health center will bill your insurance provider for the solutions you obtain. Your insurance policy card proves that you have medical insurance. It contains information that your physician or medical facility will certainly use to get paid by your insurer. Your card is additionally convenient when you have concerns about your wellness coverage. There's a contact number on it you can call for information. It might also provide essentials regarding your health insurance plan and also your co-pay for office check outs. Physicians and medical facilities commonly contract with insurer to enter into the company's"network."The contracts define what they will be spent for the care they supply. Some insurance intends will not pay anything if you do not use a network company (other than when it comes to an emergency ). So it is very important to consult the plan's network prior to seeking treatment. You can call your insurer utilizing the number on your insurance policy card. The company will certainly tell you the doctors and also medical facilities in your location that become part of their network.